Nobody really knows where the word “check” comes from. One theory traces it all the way back to chess, specifically to shah, the Persian word for “king”; by way of the idea that a check is a kind of control, a verification. Another theory is more mundane: that early banks simply numbered their drafts to keep track of them, and “check” was shorthand for checking the ledger.

Even the spelling couldn’t settle down. In the US it’s “check.” In the UK, Canada, and Australia it’s “cheque.” Both words share the same root, but they went their separate ways sometime in the 19th century — and they never came back together.

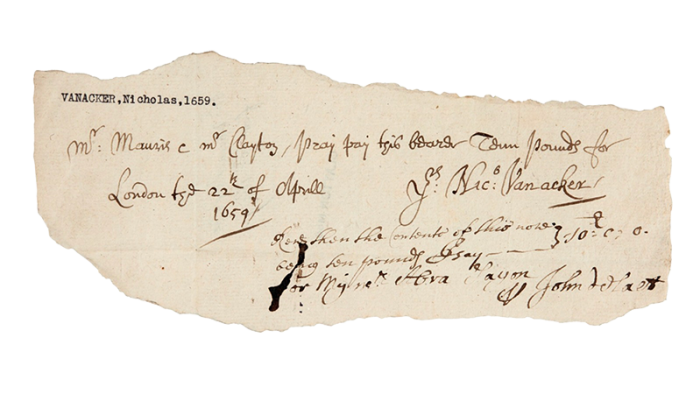

And yet, for all its quiet ordinariness, the check has a history that stretches back centuries. The oldest known example (shown below) a handwritten draft drawn on a London goldsmith’s bank in 1659 still exists. It was written for £400, a sum worth hundreds of thousands of dollars by today’s measure. Someone, somewhere, once held that slip of paper and handed it to a stranger as proof of trust. That’s all a check has ever really been.

Checks in America: A Brief History

Feel free to skip this section if you had enough of Checks history. But if you want more, then read on…

Checks have come a long way in the last ~400 years.

Checks continue to bless us with their presence into the 21st century.

Even though Checks are inefficient enough that their use keeps shrinking, they are still deeply embedded enough that they’ll probably never disappear entirely. No doubt cost has something to play here since Checks carry No interchange fees. Credit and debit card payments cost merchants 1.5–3% per transaction. Checks cost essentially nothing to accept. For landlords, contractors, and B2B businesses writing large Checks, that math matters enormously.

Accepting Checks in the 21st Century

Where Checks go, Fraud follows. Incident reports are up 134% between 2020 and 2023, suspicious activity reports climbed over 200% between 2018 and 2022, and the average victim loses nearly $1,988 per scam, almost six times the median loss across all fraud types combined. Criminals have gotten clever about it too, intercepting mail, altering payee names, washing ink — all targeting a payment method most systems ingest without a second thought.

Blindly processing Check data in 2025 without fraud Checks isn’t a workflow, it’s an open door. The good news: I have the perfect solution for you.

Bullet Proofing Your Check App

1. Capturing Checks

Nothing is more frustrating for customers who struggle to capture Checks using a mediocre camera on their mobile app (or website) that was built to capture general photos. This is where Veryfi Lens helps. Built specifically for Check capture running a machine model on the device to help with identifying a Check even if held in your hand and against any noisy background. The video below speaks for itself.

2. Extracting Check Data

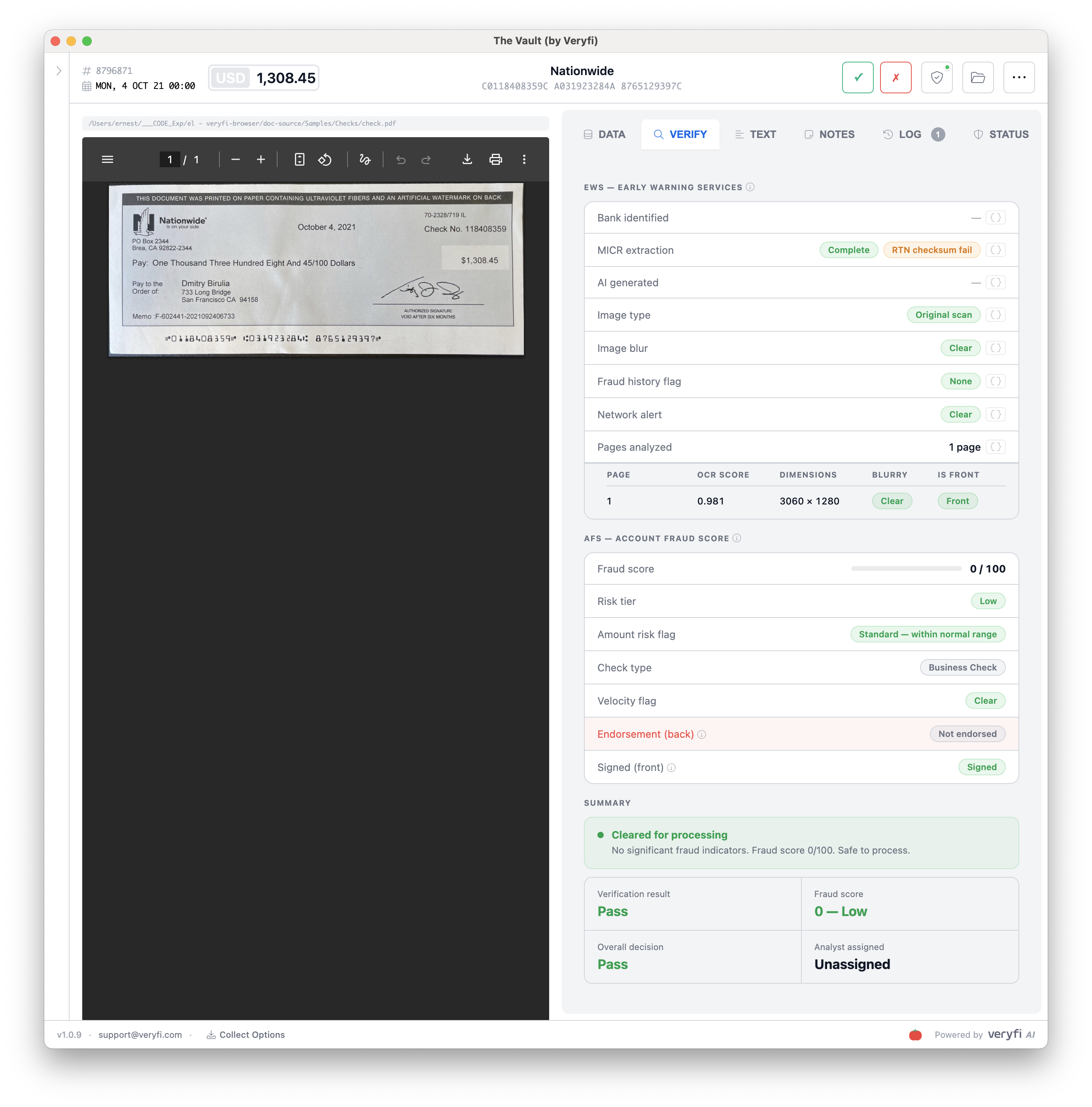

At the bottom of every check, that strange-looking row of numbers isn’t decoration — it’s MICR (Magnetic Ink Character Recognition), the banking industry’s backbone for securely routing and processing payments. It encodes the routing number, account number, and check number in ink that machines can read even if the check is crumpled, stamped, or partially obscured.

But reading the MICR line is just the start. A check also needs to be signed — on the front — and endorsed on the back before it can move through the system. Veryfi detects both: is_signed confirms the payer’s signature up front, is_endorsed confirms the payee signed off on the back. Miss either one and the check shouldn’t clear.

Then there’s the handwriting problem. Unlike invoices with printed fields, checks are filled out by humans: amounts in words, amounts in numbers, dates, payee names. The Veryfi OCR API reads all of it, then reconciles the written amount against the numeric one. If they don’t match, that’s a flag. If they do, you’re good to move forward.

Eight And 45/100 Dollars”

San Francisco CA 94158″

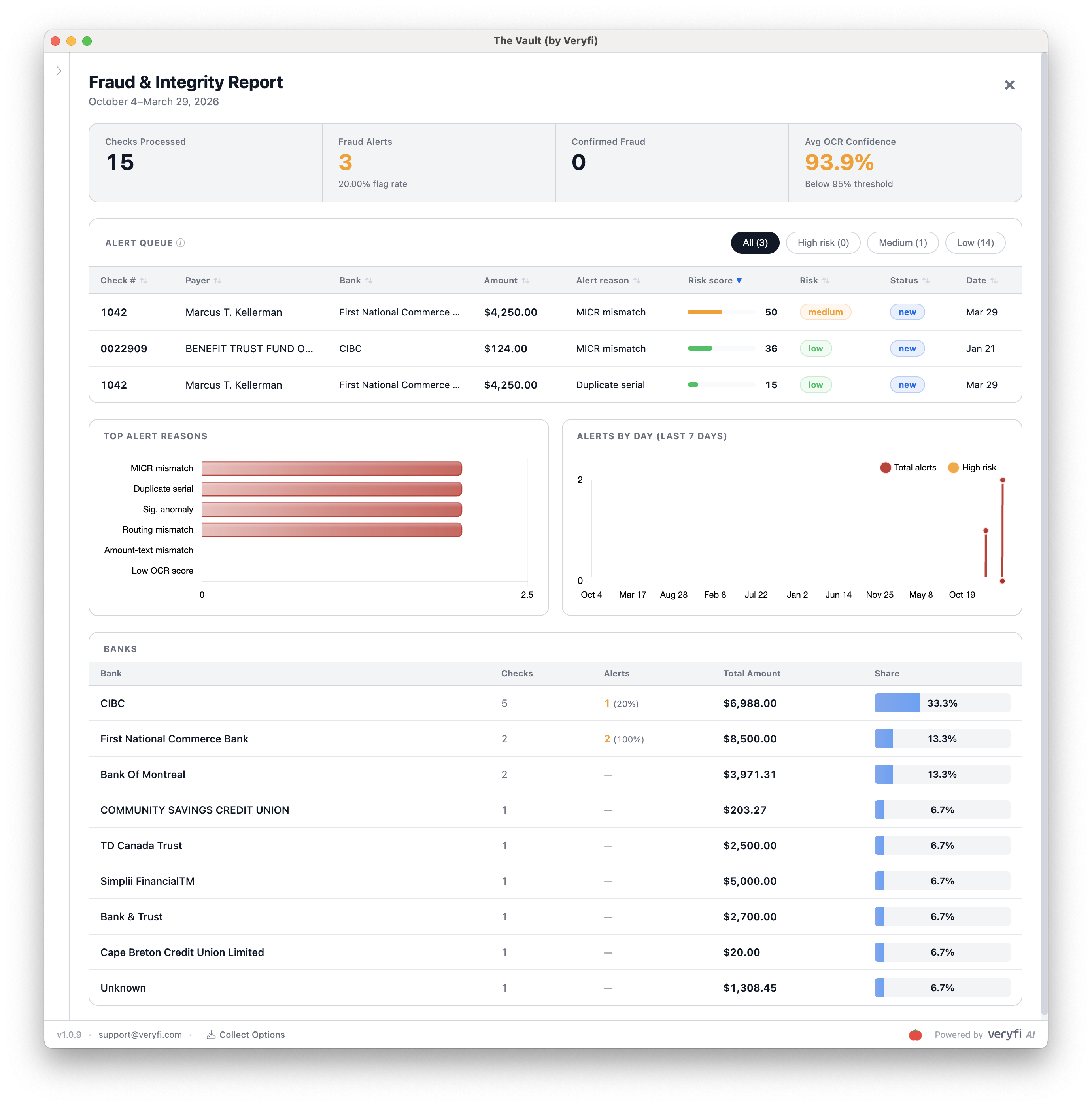

3. Catchings Threats

Processing a check is one thing. Knowing whether you should process it is another. Veryfi connects to two fraud intelligence layers that run automatically against every check:

EWS (Early Warning Services) — the risk intelligence network used by the largest U.S. banks. It flags accounts with a history of fraud, returns, or suspicious activity before you’ve committed to anything.

AFS (Account Fraud Score) — a predictive score specific to that check and account combination. Not a binary pass/fail — an actual risk number you can act on, whether that means auto-approving low-risk items or routing high-risk ones for review.

Together they give your system a second set of eyes on every transaction — the kind that doesn’t get tired at 3am.

Next Steps

If all this resonates with you then as the famous Marc Andreessen says, “It’s time to build“. Email [email protected] and have a chat with a Veryfi Expert on helping you bring light to your product with a solution that delight your customers.

Tools mentioned

- Veryfi Lens to Capture Checks

- Veryfi API for Checks OCR

- The Vault for Fraud & Integrity Reporting